A road trip to financial freedom

Exploring long-term average returns: Is 12% realistic?

By Lizelle Steyn

3 May 2026

The South African stock market returned 42% last year, a welcome surge as rare as spotting a white lion cub in the Kruger, and highly unlikely to be repeated next year. As long-term investors, we're prepared for market ups and downs, but need a reasonable average long-term return to use as the fuel of our financial plans. We can look towards the default growth rate programmed into online future value calculators - commonly ranging from 9% to 12%. Or we could look back and anchor our expectation on our existing investment's fund fact sheet, which may boast excellent double digit returns measured over many years. But fact sheets don't show performance after all platform (admin and trading fees) and adviser fees were deducted. Neither does it account for the dividends tax that is paid out of the investor's account to SARS every year.

It's the internal rate of return (IRR) we're after

At the end of every investor journey, what matters is the investor's unique IRR (internal rate of return). In other words, if you contributed to a bank account the same figures as to your investment account, and made the same withdrawals at the same time as from your investment, what rate would you need to earn on that account to end up with the same balance? That's the net performance figure that counts and for which we're trying to set a realistic assumption.

The foundation of long-term returns: it all starts with inflation

The goal of investing is to not only keep up with inflation, but to also beat it comfortably over the long term. A return of 12% may sound good, but that's no good when inflation sits at 15%.

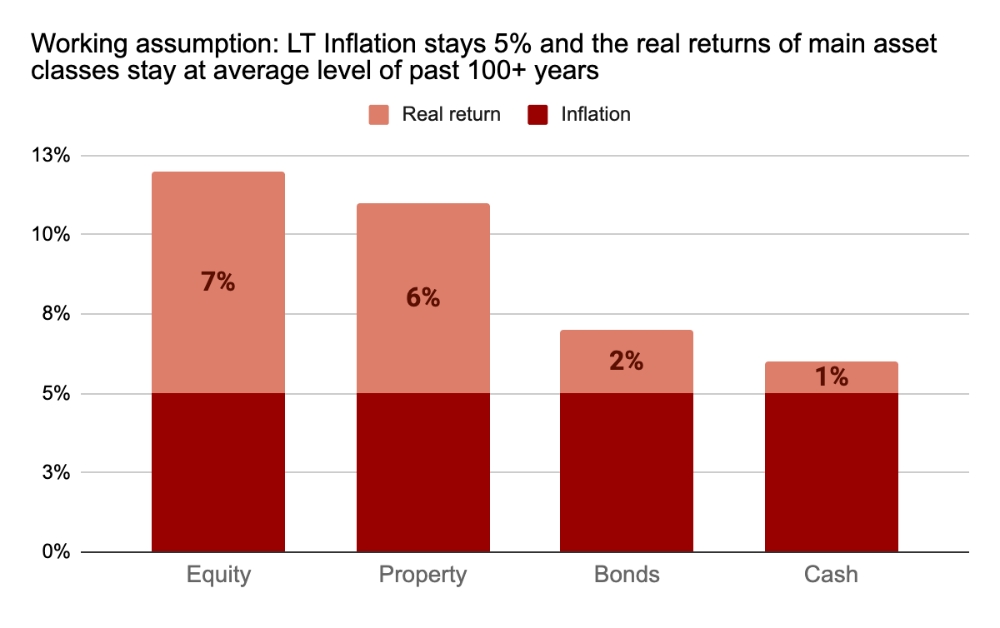

In the seminal investment book Triumph of the Optimists, the authors looked at more than 100 years of data across different countries and found that the long-term average index return per traditional asset class is actually very similar for different countries after the country's inflation rate was deducted, namely:

- equities (stocks): about 7% real return

- property: about 6% real return

- bonds: about 2% real return

- cash: about 1% real return

To work out what performance to expect from the top performing main traditional asset class - equities - we need to start with the expected inflation rate. What would that be for South Africa going forward? From 1980 to 1994 SA inflation stayed above the 10% level. Over the past 20 years, our inflation rate has been about 5% on average. The new inflation target of the SARB is 3%. Whether this is sustainable over the long term with the current geopolitical tension remains to be seen. For this exercise, we're sticking with 5%, as experienced and proven over the past 20 years. This might turn out to be too high, but for now it's the long-term figure that feels real.

If we expect inflation of 5% going forward, and equities have always delivered around 7% in real returns on average, we can reasonably expect average stock market performance of 12%.

Source: Triumph of the Optimists

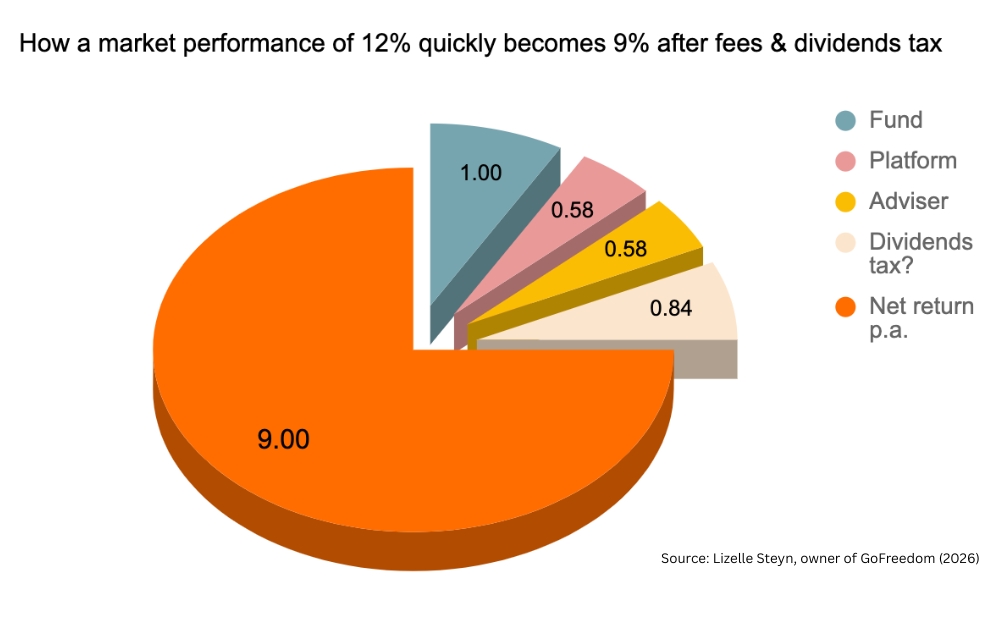

But only a small fraction of investors achieve or beat the market's performance

It's important to distinguish between market and portfolio performance. Not even investors in index funds can achieve the performance of the market. At least one of the following components will reduce the anticipated average equity market performance of 12%:

- Fees at a platform level, e.g. admin fees and/or ETF trading fees plus VAT

- Fees at a fund (unit trust or ETF) level

- Adviser fees, if appointed

- Dividends withholding tax (DWT) paid directly to SARS by the financial institution on behalf of the investor every year

| Type of deduction | Size of deduction |

|---|---|

| Platform fees | In SA, this can range from about 0.2% to 1.5%. Median platform fee of 0.5% + VAT. |

| Fund fees | Huge range, from about 0.2% to more than 3%. Let's assume a combination of index and actively managed funds, with a resultant average fund fee of 1% |

| Adviser fees | This is negotiable, but the median adviser fee is 0.5% + VAT |

| Dividends withholding tax | Dividends now make up 30-40% of the return of an equity portfolio (Source: Allan Gray). Without going into the detail of the calculation: If dividends form on average 35% of the gross return of a portfolio, the resultant average impact of DWT is to lower the return by 0.84%. Not applicable to a TFSA. |

Because of the list of "deductions", most investors' return experience would be lower than the figures in the chart above.

Different layers of fees and dividends tax combined could easily take a 3% bite out of a 12% stock market performance

Out of scope but not off the radar: capital gains tax

This exploration of what investors can realistically expect in terms of an average annual portfolio return doesn't include the once-off impact of capital gains tax at the end of the investment period. It's not applicable to any equity funds inside a tax-free savings account or a retirement product. For all other (discretionary) investments, it's worth considering - once the investment has been growing for a few years - withdrawing an amount just large enough to have a capital gain of R50,000 per tax year, as this is currently the annual CGT threshold under which no CGT is payable. That withdrawal must then be re-invested as soon as possible, "resetting" the capital base cost at a higher amount every year.

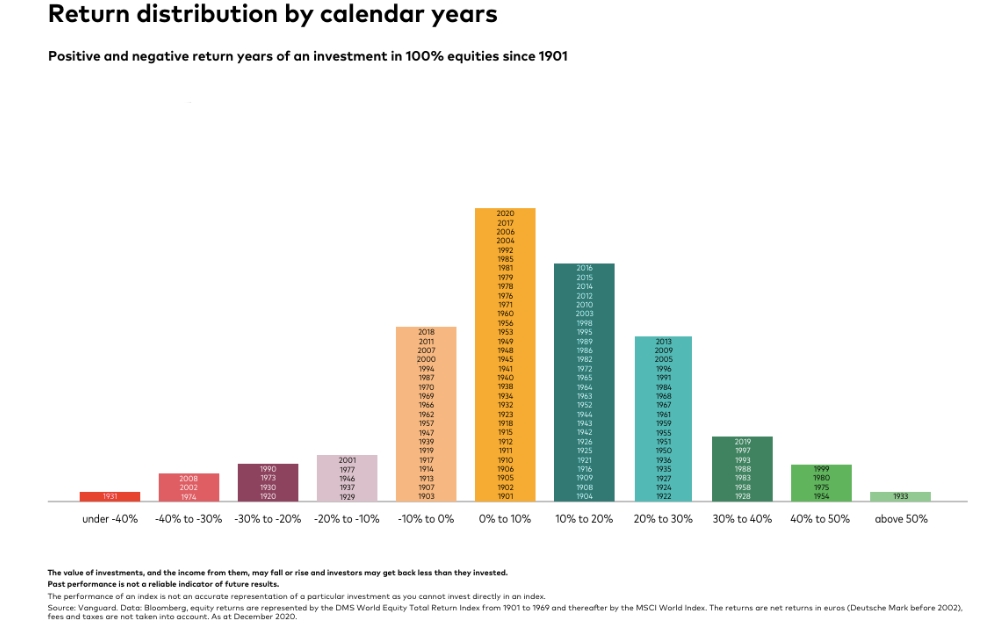

Stock market returns don't arrive in equal measure

When we choose to invest 100% in equities, we strike a deal with the stock market: we're willing to stomach sometimes severe ups and downs to harvest the potentially higher average return over the long term. The chart below shows that annual returns in the 0-10% range is the most common, but there are also many years with returns ranging from -10% to 0% (and a few years of much worse drawdowns).

Source: Vanguard (2021)

Some of the worst calendar-year investment returns in the past 20 years:

| Asset class | Worst calendar year performance over the past 20 years |

|---|---|

| SA All Share Index | -23% (2008) |

| US S&P 500 index | -38% (2008) |

How do you increase your chances of a higher return?

Fortunately, there are ways to decrease the chunk of fees and dividends tax on an equity portfolio, bringing you closer to the 12% the stock market can potentially offer long-term investors.

| Zero platform fee | For unit trust investors, it's possible to cut out platform fees by investing directly with the unit trust management company. Coronation, Nedgroup Investments and 10x are examples of well-known unit trust businesses. The downside is that you're limited to only their unit trusts. For ETF investors, Fynbos offers a TFSA with zero platform fees and very low charges to buy and sell your chosen ETF. |

| Lower fund manager fee | The average fund manager fee can be reduced by only investing in index-tracking ETFs or unit trusts that track the most popular main equity indices locally and internationally. The Satrix 40 ETF and the Sygnia itrix S&P 500 ETF are examples of ETFs that normally charge no more than 0.2% p.a. |

| Negotiable adviser fee | It's possible to invest without an adviser and that's normally perfectly fine for young DIY investors who are investing without needing the money within, say, 10 years. Investors closer to retirement will benefit from professional advice and can negotiate the % or ask for a flat-fee consultation. |

| Zero dividends tax | There is no dividends tax within a tax-free savings account. The same applies to retirement products, but unfortunately retirement funds don't allow a 100% allocation to equities. |

| Ideal investor behaviour | Investors who stay invested through market crashes have better results than those who try to time the market. |

| Higher octane, riskier equity | Consider including private equity (companies not listed on a stock exchange) or equity hedge funds (equity funds that use additional finance to "amplify" the return) in your portfolio. Make sure to only deal with reputable fund managers with a substantial track record. And be aware that the additional finance (basically a loan) that the hedge fund manager brings in, could also result in amplifying a potential negative return. |

Investors willing to do their homework, who hunt for the lowest fees, accept some of the limitations that go with these, and invest consistently through stock market ups and downs are the ones who might just achieve those average annual returns of 12% over time (assuming long-term inflation stays at 5%).