A road trip to financial freedom

2022 Financial freedom update

By Lizelle Steyn

3 January 2023

There are many metaphors for how you treat your money. You could flush it all down the drain as soon as it comes in. Or use it to create experiences that lead to a nice album packed with memories. But either way, money would just come and go and never stay for long. That was me in my 20s.

You could keep on feeding a big secret hole in your backyard and every few months dig it up and wallow in your money but still end up feeling it's never enough. You always have to feed the 'hole' with more money. That could have been me in my 40s had I not come across the concept of FIRE. Being able to quantify how much is enough has brought clarity and peace to my relationship with money.

One of the metaphors that works for me is a jar. The 4% rule used by the FIRE community means the jar needs to be able to hold 25 times your annual expenses, and once it's full it's no longer necessary to save more money. In June 2019 when I started this blog, the jar was 52% full - I was about half-way on my journey to financial freedom – having enough in investments to keep a roof over my head and food on the table for life.

Financial freedom starts with taking control of your expenses

Financial freedom can only be reached if you can control your expenses and your needs. That's not so easy, though. Especially if you have anyone in your household who hasn't yet seen through the brainwashing of the ad industry, which has been pushing the more-more-more agenda on a large scale since the 1920s and keeping people in soul-destroying jobs, unable to step off the hedonic treadmill. I've been fortunate in that my expenses have come down slightly since 2019 due to no international travel and moving to the countryside with no Woolies nearby.

My top 10 expenses end of 2022 (average per month)

- Food and groceries: +/- R3 500

- New home and garden stuff: +/- R2 800

- Medical aid: R2 180

- Weekends away: R2 000

- Municipal account: +/- R1 300

- Gifts: +/- R1 200

- Cleaner's pension: R900

- Critical illness insurance: R794

- Electricity: R770

- Retreats, workshops, classes and books: +/- R750

Every year I look at this list and ask myself if it reflects what's important to me right now or do I need to make a few tweaks? In 2022 I spent quite a lot on the home and garden front, from drawing up plans for adding a bedroom to buying more planter boxes and a water tank. Setting up my new spot enjoyed priority during lockdown but I can feel things are shifting again. I've decided there will be no construction in 2023 and that I'm happy with what I have - for now. The new garden beds are set up and I just need to plant new annuals every season. Maybe some of the home budget can go instead towards a little more travel and workshops/learning in 2023.

I also invested money during the year in my employer's provident fund and across different accounts with Easy Equities, but they’re not listed as expenses; that's building the balance sheet (filling the jar).

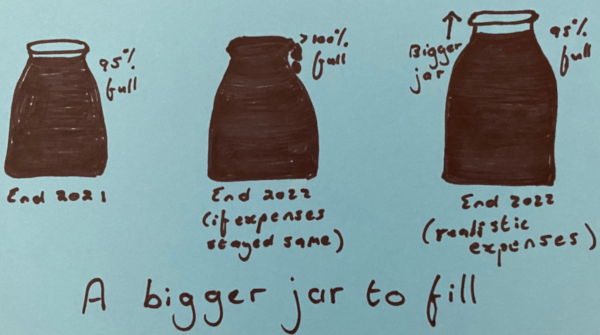

What's happening inside the jar?

A year ago my financial freedom jar was 95% full. During the year my portfolio grew by about 7%. Had my target amount stayed the same, I would have made my target set in 2019 by the end of 2022. The jar would have been full. But I have to be honest, I cannot comfortably live on 4% of my original 2019 target now; there's been some 'needs and wants' creep. For example, if I come across a workshop that really speaks to me, I want to be able to do it, even if it's in another country. My budget needs to expand and I had to adjust my desired drawdown by R2 000 a month, which means I now have a slightly bigger jar to fill. Which means I end 2022 at 95% full, the same as last year.

How did my funds perform?

Like most South Africans, my offshore funds show single-digit negative returns and my SA funds modest positive returns for 2022. Worst performers inside my portfolio were the index-tracking Satrix MSCI World and my small exposure to cryptocurrencies. Best performers were the Allan Gray Equity Fund and the Peregrine Capital Pure Hedge Fund. One year is a very short period, though, when you're a lifetime investor. Through all the cycles, every region and every good fund management house gets its year of outperformance - and underperformance. It's the 10-year performance figures that really matter. During some 10-year cycles offshore outperforms and during others local funds do better (like 2001 - 2010). There are only a handful of funds in my portfolio in which I've been that long, with the Orbis Global Equity Fund the best of the lot as measured over the most recent 10 years. It hasn't shot the lights out over this period and there will always be competitor funds that perform better, but it's beaten inflation by several % and grown what's in the jar. This is after all a road trip and not a sprint towards financial freedom.